There's a lot to like about dividends. Getting a regular check in the mail from the companies you own is a testament to their discipline, the health of their business, and their confidence in its future. But the stock prices of firms with stable cash flows tend to be more sensitive to fluctuations in interest rates than those with more-volatile cash flow streams. Here, I'll examine this relationship in more detail to understand whether it's something investors should sweat over.

Asset Prices and Interest Rates Down by the Schoolyard

Imagine interest rates and asset prices as kindergarten pals mounted on either end of a seesaw in the schoolyard. As rates rise, asset prices tend to fall. When rates come down, asset prices get a lift. These ups and downs are most pronounced for long-lived assets that produce predictable cash flows, like long-duration bonds.

While their cash flows may not be as stable or reliable as bonds', dividend-paying stocks tend to exhibit a similar relationship with interest rates. Historically, the highest-yielding stocks have underperformed those that either don't pay dividends or have lower yields during periods of rising interest rates. The inverse has been true when rates have fallen: High-yielding stocks have trounced their less-generous peers.

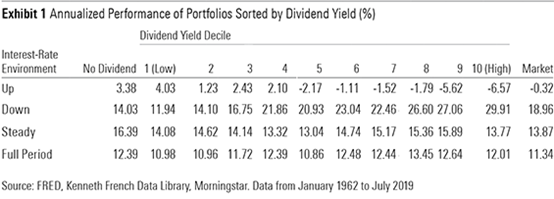

Exhibit 1 illustrates this relationship. I looked at monthly changes in the 10-year Treasury yield dating back to 1962. In defining interest-rate environments, I counted the 25% of greatest month-to-month increases in 10-year yields as "up" periods, the middle 50% as "steady," and the 25% greatest month-to-month declines as "down." Using data from Kenneth French's Data Library, I examined the performance of U.S. stocks across each environment, breaking the universe into dividend payers and nondividend payers and sorting based on dividend yield.

The performance differences among stocks in the highest- and lowest-yielding deciles are pronounced during periods when rates are rising or falling. However, those spreads narrow significantly when rates are steady. And over the full period, the performance differential between high- and low-yielding stocks narrows further still.

Exhibit 2 features the results of a regression analysis I ran on each stock portfolio's returns. I used the market risk premium and monthly changes in the 10-year Treasury yield as explanatory variables. The coefficients in the table indicate how sensitive each portfolio is to changes in the variable in question. A positive value indicates that the two tend to move in the same direction. A negative value indicates an inverse relationship.

Equity risk was least pronounced among those that show more bondlike characteristics--the ones that throw off regular cash flows to their investors. These firms tend to be mature, and their businesses tend to be less cyclical than most. These factors allow them to commit to paying and--in some cases--growing their dividends over time. The market tends to punish firms that cut their dividends, so firms with more-volatile cash flows are likely to be more conservative with their dividend policies.

While higher-yielding stocks tend to have a low degree of sensitivity to market movements, they have a strong negative relationship with interest rates. That's no coincidence. Because they tend to have more-stable cash flows, higher-yielding stocks tend to have less growth when the economy is doing well to offset the negative impact of rising rates than lower-yielding stocks. Conversely, they get more of a lift when interest rates fall.

In part 2 of this article, we will continue to explore the relationship between dividend yields and interest-rate sensitivity by connecting the dots with companies’ fundamentals.