In part 1 of this article, we looked at some relationships between market-cap weighting and momentum strategy. Here, we will explore “momentum” further.

Measuring the Market’s Momentum

Whether or not market-cap weighting captures momentum depends in part on how you define momentum. Few would argue that markets don’t experience momentum. But that doesn’t mean that the market itself is a momentum strategy.

The most common measures of momentum anchor on price changes. They look for the stocks whose prices have been going up (or down) the fastest. The most widely accepted measure of momentum in academia looks at returns over the past 12 months, excluding the most recent month (because returns over the past month have a tendency to reverse over the next month). The academic momentum factor (MOM) goes long those stocks showing the strongest positive momentum and shorts those showing the strongest negative information.

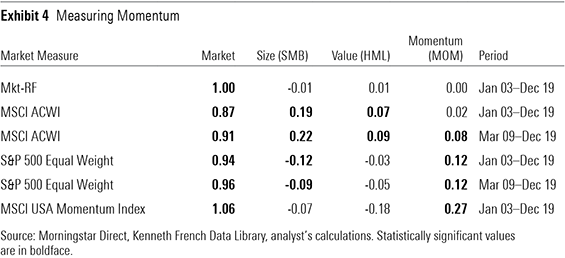

Exhibit 4 contains the results of a handful of regression analyses I ran to assess whether the market, proxied by Vanguard Total Stock Market Index, exhibits any evidence of exposure to the academic momentum factor. The first row represents the regression results for the period from January 2003 through December 2019 using the standard academic definitions of the market, size, value, and momentum. As you can see (and as I said before), the market is the market. This regression shows that the Vanguard fund showed no significant exposure to any of these nonmarket factors during this period. Of course, I’ve regressed a market proxy against the market itself here, so the result is unsurprising.

But what if we define the market differently? The second and fourth rows of Exhibit 4 contain the results for a pair of regressions where I swapped in a pair of different market measures: the MSCI All Country World Index and the S&P 500 Equal Weighted Index. Using the former can give us a sense of whether the U.S. market has shown momentum versus the broader global stock market. The latter can tell us something about whether weighting stocks by market cap introduces a momentum tilt. The regression result using the ACWI as a market proxy shows a touch of momentum in the mix, though it is statistically insignificant. The regression that uses the equal-weighted S&P 500 as a market measure shows a modest and statistically significant loading to momentum, perhaps lending some credence to the argument that market-cap weighting is a closet momentum strategy.

These regression results will vary across time periods. The third and fifth rows in Exhibit 4 show the Vanguard fund’s factor loadings as measured against the ACWI and equal-weighted indexes, respectively, from the market’s post-crisis trough through the end of 2019. In this case, both regressions show a statistically significant loading to the standard momentum factor.

Does this further bolster the notion that market-cap weighting is a momentum strategy? Maybe. There’s no changing the fact that the two are definitionally different. The market is the market. Momentum strategies own a smaller subset of the market, weight stocks by measures other than price, and turn over far more frequently. As you can see in the final row of Exhibit 4, a more-focused momentum strategy (as represented here by the MSCI USA Momentum Index) will likely show a far greater weighting to the standard momentum factor. Aside from definitional differences, there are more fundamental questions about momentum that need to be addressed before reaching a verdict.

It’s Fundamental

More recent research on momentum has linked the phenomenon to fundamentals. In a 2015 research paper, Robert Novy-Marx uncovers the explanatory power of earnings momentum, as proxied by earnings surprises.[1] He concludes, “After controlling for fundamentals, past performance does not provide significant additional information regarding expected returns. Fundamentally, momentum is fundamental momentum.”

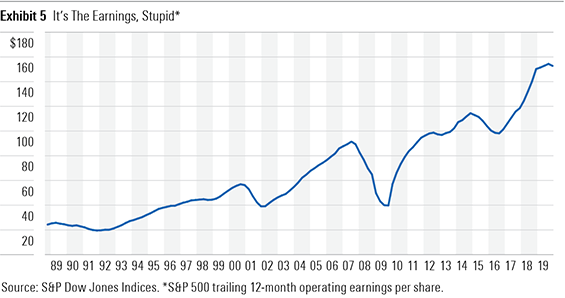

Framing momentum as a factor of fundamentals makes the case for market-cap weighting being a momentum strategy far more compelling. Over long horizons, market-cap-weighted indexes will naturally accord greater weightings to stocks that have sound fundamentals and lower weightings to those whose earnings are declining. The characteristics of market-cap weighting outlined above will therefore naturally track the market’s earnings cycle (see Exhibit 5). Couched in terms of fundamentals, I think that there is a strong case to be made for market-cap weighting being a momentum strategy.

Conclusion

Market-cap weighting is a form of momentum strategy—just not in the way that many think. Under certain circumstances, a cap-weighted index can show slight loadings to the standard academic definition of price momentum, but that’s insufficient evidence. The case becomes much stronger when we link the manner in which market-cap-weighted indexes evolve over a market cycle back to fundamentals. In my opinion, fundamentally, market-cap weighting is, more intuitively, a means of leveraging fundamental momentum.

[1] Novy-Marx, R. 2015. “Fundamentally, Momentum is Fundamental Momentum.“ NBER Working Paper No. 20984. http://rnm.simon.rochester.edu/research/ FMFM.pdf