The first quarter of 2021 was a challenging one for the performance of investments screened on environmental, social, and governance (ESG) criteria. Why? The best performing sector in global equity markets was energy, while technology was the worst. ESG screens tend to favour technology and avoid the carbon-intensive energy sector.

Reflecting ESG’s first-quarter struggles, Morningstar’s range of ESG-screened indices generally underperformed their broad market equivalents in the first quarter, with some important exceptions. For sustainable investors, it’s a reminder that any deviation from a broad market portfolio will inevitably go through cycles. Sustainable investments performed well as a group during the growth rally of recent years but will remain challenged if the energy sector continues to lead the market.

How widespread was ESG’s underperformance? During the first quarter, just 24% of Morningstar’s ESG-screened indices beat their broad market equivalents.

- Five of the 21 members of the Morningstar Sustainability Index Family outperformed in the first quarter.

- None of the Morningstar Sustainability Leaders Indices or the Morningstar Renewable Energy Indices outperformed during the quarter.

- Only four of 10 members of the Morningstar Low Carbon Risk Indexes beat their non-ESG counterparts in the first quarter.

Long-term, though, the investment case for ESG is encouraging. That fact that ESG screens have led to resilience in recent down markets, driven by the relationship between sustainability and attributes like corporate quality and financial health, supports the view that ESG risk is material. The persistent perception that sustainable investing requires a return sacrifice is misplaced.

ESG in a Value Rally

For years, the market’s preference for growth stocks has benefited sustainable investments. Technology-related companies have led global equity markets for more than a decade, while energy in particular has lagged. When company-level ESG Risk Ratings from Sustainalytics are aggregated to the sector level, technology and tech-related companies as a group carry far less ESG risk than energy, utilities, and basic materials. Nvidia (NVDA), ASML (ASML), and Keyence (6861) are far more common constituents of ESG-screened portfolios than Royal Dutch Shell (RDSA) or Exxon Mobil (EXOM).

Against this backdrop, our analysis of Morningstar’s ESG-screened indexes found that 52 of 69 (75%) bested their broad market equivalents in 2020, while 88% outperformed for the five years through the end of 2020.

But lately, the market’s rotation to value and the resurgence of the energy sector left ESG out of step. As Russel Kinnel observed, equity market leadership began to shift in September 2020. November saw an acceleration of the trend when Covid-19 vaccines and US presidential election results lifted hopes of an end to the coronavirus pandemic and a stimulus-fueled recovery. But it wasn’t till the first quarter of 2021 that value stocks opened up a more significant lead.

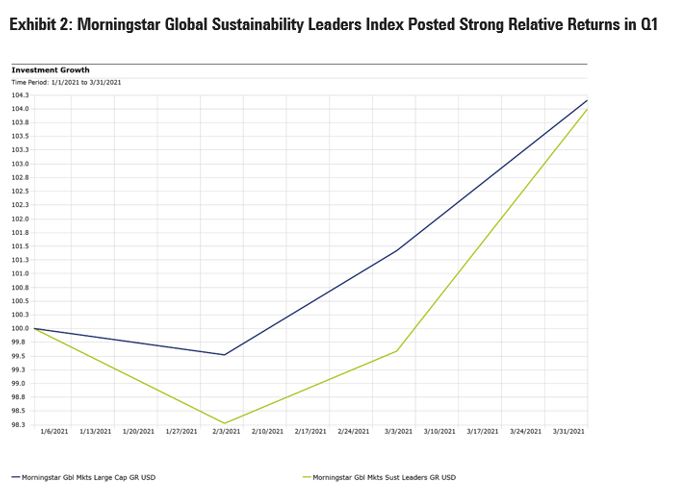

For example, the Morningstar Global Markets Sustainability Leaders Index, which is concentrated, unconstrained, and maintains high ESG standards, returned roughly 3.9% for the first quarter compared with 4.2% for the large-cap equity segment from which it is drawn.

What drove those returns?

- The ESG-screened index’s below-market exposure to energy detracted 27 basis points from relative returns in the first quarter…

- …while the index’s above-market technology weight contributed 26 basis points to underperformance.

- Top 10 constituents Adobe (ADBE) and Salesforce.com were in negative territory.

- Energy stocks not included in the ESG index, like Exxon, Canadian Natural Resources, and Rosneft, all gained more than 25% in the first quarter.

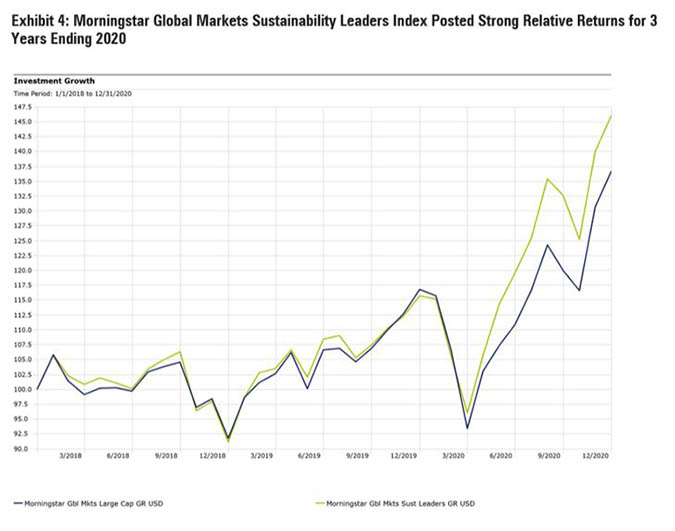

But to keep the first quarter trends in context, the Global Markets Sustainability Leaders Index averaged a 13.5% annual return for the three years to the end of 2020, while its equivalent market segment returned 11%. The biggest contributors to the outperformance were above-market technology exposure and below-market energy

exposure.

This isn’t the first time a value rally has treated ESG unfavorably. In the fourth quarter of 2016, Donald Trump’s election victory was interpreted by the market as a boon for economically sensitive sectors that would benefit from spending, protectionism, and a regulatory rollback. Energy and basic materials soared. Only nine of the 21 members of Morningstar Sustainability Index Family, which was launched in mid-2016, outperformed during the value rally of 2016’s fourth quarter.

Bright Spots for ESG in the First Quarter

The full story of ESG in the first quarter contains nuance though, as is always the case. First, it must be pointed out that some ESG-screened indices overcame challenging sector dynamics and outperformed regardless.

The Morningstar Global Markets Sustainability Index is one prominent example. It keeps its sector weights roughly in line with the market while emphasising companies with lower ESG risk, and posted a strong quarter thanks to the stocks it both included and excluded. Above-market exposure to Microsoft and Tencent, which had strong quarters, helped. Not including Amazon.com (AMZN), and Tesla (TSLA), both of which struggled, helped the ESG index.

Why aren't Amazon and Tesla in the Global Sustainability Index? Neither made the inclusion threshold based on Sustainalytics’ assessment of their ESG risk. Amazon falls short especially on the social side, while Tesla, among other things, is quite carbon-intensive in its operations, even if its product is environmentally-friendly.

But to say that ESG is all about heavy technology and light energy is a caricature. There are plenty of technology and tech-related companies that don’t score well on ESG, while some companies within the energy, utilities, and materials sectors manage their ESG risk well.

Some of Morningstar’s ESG-screened indexes that outperformed in the first quarter put more emphasis on social factors than environmental. For example, the Morningstar US Gender Diversity Index employs diversity, equity, and inclusion screens and was actually heavier on energy and lighter on technology than the market. Technology companies, generally speaking, are not exemplars of gender diversity but some energy companies score well.

ESG for the Long-Term

Ultimately, it’s key not to get too hung up on short-term performance fluctuations. No investment strategy works all of the time. ESG screens cause divergence from the market, which will inevitably lead to good performance in some environments and underperformance in others.

ESG screens have led to resilience in down markets, even in brutal downturns since as March 2020. Morningstar and Sustainalytics have documented links between ESG and factors like corporate quality and financial health. So long-term, there are reasons for investors to be encouraged about the prospects for ESG investments in their portfolios.