Commodities are often touted for their diversification benefits. Because their prices mainly depend on the balance of supply and demand, they often show very low correlations with other asset classes.

Commodities are traditionally defined as raw materials or other basic ingredients used in manufacturing and industrial processes. As basic materials, they're essentially interchangeable with other commodities of the same type. In addition to their diversification benefits, commodities can also be a useful hedge against inflation. Commodities themselves are a major part of most inflation indexes, and it makes sense that their prices tend to rise when inflation is increasing. Some commodities also show seasonal price movements, which can affect returns over shorter periods.

But in our recent examination of asset-class correlations, the "2021 Diversification Landscape," we found that commodities have been moving more in tandem with other asset classes in recent years.

2020 Correlations for Commodities

Commodities provided a measure of protection during the COVID-19-driven bear market in early 2020, but anything energy-related suffered even sharper losses than the overall market as the price of oil collapsed. As a result, the Morningstar WTI Crude Commodity ER Index dropped 54.8% in the first quarter, and the Morningstar Energy Commodity TR Index shed 48.9%. Other commodities held up considerably better.

Diversified commodity indexes vary significantly, and the level of exposure to energy often drives their results. The Morningstar Long-Only Commodity Index has a 40% weighting in the energy sector but also measures the performance of futures contracts on other commodities, including agriculture, livestock, and metals. The index was down about 25.5% for the quarter. Copper also held up relatively well, but gold excelled with only a 2.3% loss.

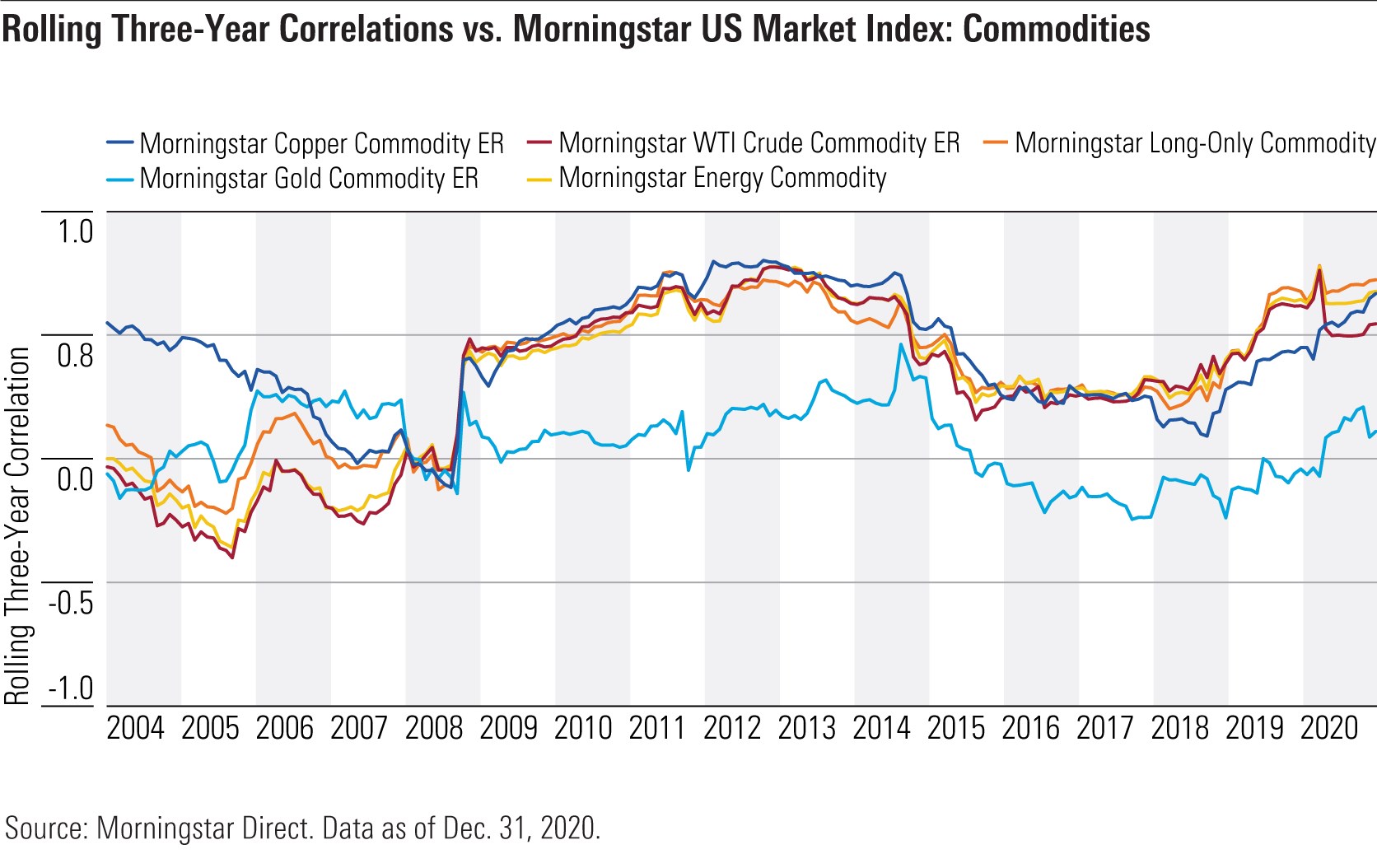

For 2020 overall, returns (and correlations) showed a similar pattern. Energy-related benchmarks showed the highest correlations with the broader equity market, and correlations for copper also increased relative to previous levels. Gold's correlation with the overall equity market edged up from levels shown in previous years but remained quite low, at 0.22.

Longer-Term Trends for Commodities

Over time, correlations for most commodities have generally increased versus the Morningstar US Market Index. The Morningstar Long-Only Commodity TR Index, for example, showed a correlation of 0.74 when compared against domestic stocks in 2020, up from 0.43 over the trailing 20-year period. This partly reflects lower collateral yields (which are based on short-term Treasuries) over the years and the growing contribution of the spot and roll-yield components in these benchmarks' overall returns--with the latter two being more equitylike.

Another possible explanation is increasing asset flows from institutional investors. Paradoxically, investors seeking out diversification may have caused commodities to behave more like traditional financial assets. As mentioned above, gold has also been moving slightly more in tandem with the equity market, but its correlation coefficient has remained relatively low.

Historically, commodities have generally been a strong hedge against inflation, but it's not clear if this will hold true in the future. Over the past several years, major commodity indexes have actually had a slight negative correlation with inflation. However, commodities have continued to show negative correlations versus market volatility (as measured by the CBOE VIX Index). Other commodities (except for gold) have also had negative correlations with bond market indexes, making them a potentially useful hedge during periods of rising interest rates.

Portfolio Implications

As investors increasingly treat commodities as financial assets, their value as portfolio diversifiers has diminished. Gold is a notable exception and should continue to fill a valuable role as a buffer against equity market volatility. Other commodities, meanwhile, can still provide some diversification benefits for bond-heavy portfolios. It's also worth noting that the way investors access commodities plays a major role in the potential outcomes. Roll yield, seasonality, and implementation decisions can all have a significant impact on results.

©2021 Morningstar. All rights reserved. The information, data, analyses and opinions presented herein do not constitute investment advice; are provided as of the date written, solely for informational purposes; and subject to change at any time without notice. This content is not an offer to buy or sell any particular security and is not warranted to be correct, complete or accurate. Past performance is not a guarantee of future results. The Morningstar name and logo are registered marks of Morningstar, Inc. This article includes proprietary materials of Morningstar; reproduction, transcription or other use, by any means, in whole or in part, without prior, written consent of Morningstar is prohibited. This article is intended for general circulation, and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Investors should consult a financial adviser regarding the suitability of any investment product, taking into account their specific investment objectives, financial situation or particular needs, before making any investment decisions. Morningstar Investment Management Asia Limited is licensed and regulated by the Hong Kong Securities and Futures Commission to provide investment research and investment advisory services to professional investors only. Morningstar Investment Adviser Singapore Pte. Limited is licensed by the Monetary Authority of Singapore to provide financial advisory services in Singapore. Either Morningstar Investment Management Asia Limited or Morningstar Investment Adviser Singapore Pte. Limited will be the entity responsible for the creation and distribution of the research services described in this article.